Should you exercise your stock options?

Don’t drink the kool aid – think like an investor.

👋Hi, it’s Greg and Taylor. Welcome to our newsletter on how to make high-stakes professional and personal decisions in your 30s and beyond.

Read time: 10 minutes

–

It’s the most common question I get from startup employees in Silicon Valley: “I’m leaving my startup – should I exercise my options?”

90% of the time, I say no.

For most employees, the future value of stock options in startups is a lie perpetuated by founders, CEOs, and investors. The lie: these options will make you real money. More likely, they will be worthless OR they will cost you money.

There are exceptions like Doordash, Datadog, and Okta. But these are exceptions. For the rest of us, there is a less than 10% chance your options will be worth anything.

My quick rule of thumb: Unless the startup is later stage with a good chance to get to at least $100 million in annual revenue, don’t exercise. Startups with less than $100 million in revenue rarely exit at valuations robust enough to make the stock most employees get worth anything. And even high-fliers like Doordash and Stripe can see their IPOs delayed – which means you will have to wait for your check.

In deciding whether to exercise options, most of us are imagining this nightmare scenario: we leave the company, don’t exercise, and 5 years later we’re seeing Instagram posts by former coworkers buying new homes after the company IPO.

Don’t make the decision based on FOMO. Here’s how to make it the smart way.

– Greg

The framework: Evaluate your company as an investor

There are only two scenarios when you might consider exercising your options:

You're leaving your company

You’re still at a company, but think it will exit in the next 1-3 years

Scenario 2 is rare – you need very strong evidence your company will IPO in the next 1-3 years, and you’re exercising to unlock capital gains tax (rather than income tax). If you think you’re a candidate for scenario 2, email us.

Most of us, if we work at startups, will face scenario 1 at some point. So that’s where we’ll focus.

When you leave a startup, you’re usually forced to decide whether to exercise or not. Most companies have 90-day exercise windows, meaning you have 90 days to decide to purchase your options, or they go back to the company.

If you don’t exercise, you lose the options and won’t make any money if the company exits later.

If you exercise, you’re writing a check in the hopes you’ll get a return later. That’s an investment. So you should decide like an investor would. Here’s how:

Step 1: Gather information on your stock options

Step 2: Make assumptions about your potential valuation

Step 3: Calculate your potential return

Step 4: Discount based on exit likelihood

Step 5: Evaluate your investment

Step 1: Gather information on your options

First, you need four data points.

1. Strike price – the price you can purchase your options at. You should be able to find this in Carta or your original option grant letter. This price never changes – it was set at the time you were granted the options.

2. Vested shares – the number of your shares that will have vested (and therefore are available for you to buy). You can find this in Carta.

3. Shares outstanding – the number of total shares that exist in the company. You’ll need this number to calculate the expected future price per share, and therefore understand your return. Ask your manager, HR, or CFO.

4. Preference – the amount of preferred venture capital invested in your company. This is a type of equity reserved for venture capital investors, and when your company gets sold, preferred capital gets paid back first. This is critical to understanding your potential upside. If your company gets acquired for $100 million, but investors put in $40 million of preferred capital, that $40 million gets paid back before any returns are distributed. So if you owned 1% of the company, you’d get paid 1% of $60 million, not 1% of $100 million.

Ask your manager, HR, or CFO for this number. You might have to persist to get this data, as your CEO is more inclined to maintain the illusion of a future payday rather than enable employees to do their own math. But even if it’s not commonly shared, it’s totally reasonable for you to ask.

Step 2: Make assumptions about your company’s potential valuation

In this step, we’ll approximate how your company will be valued upon exit. Private companies are usually valued as a multiple of revenues. For example, the average revenue multiple for a B2B SaaS company exiting in 2023 was 5.1x revenue, meaning if a company was making $10 million in annual revenue, it was usually sold for $51 million (or 5.1 x 10 million).

To approximate your future valuation, we’ll first make some assumptions about future revenue and future multiples.

To assume future revenue, write down:

Your company’s current revenue

Your company’s current annual growth rate

An assumed growth rate over the next 3-5 years

Your potential company revenue in 3-5 years (use the equation below)

To assume future revenue multiples, write down:

Revenue multiples for similar companies to yours right now

Then multiply your future company revenue by your expected revenue multiple to get your potential valuation.

These are all assumptions, but they’ll give you a better sense of your potential return in a minute.

Step 3: Calculate your potential return

Next, we’ll estimate your potential returns based on your three potential valuations (conservative, average, and high).

First, calculate the expected future value per share: Take your three potential valuations, subtract the preference, and divide by the number of shares outstanding.

Second, calculate your potential return: Take the expected future value per share, subtract your strike price, and multiply by the number of shares you’re planning (and able) to buy.

You’ll end up with three versions of your potential return, based on whether your company sees a conservative, average, or high multiple.

There’s a lot of math here – use our Options Scenario Calculator to do this math for you. The important thing is that you gather the data, make some assumptions, and get a few scenarios to evaluate.

Step 4: Discount based on exit likelihood

Even if your company has a high valuation, it doesn’t guarantee an exit (IPO or acquisition). Only 10-16% of startups will ever exit (and therefore liquidate their options). Vegas has better odds.

As an investor, discount your exit scenarios by the likelihood they happen. Use this TechCrunch data to approximate for exit likelihood by funding stage.

You can select your company’s stage in our Options Scenario Calculator, or do the math yourself. Multiple your potential return by the likelihood of exit for your company. For example, if you’re at a Series C company, multiply your potential outcomes by 15%.

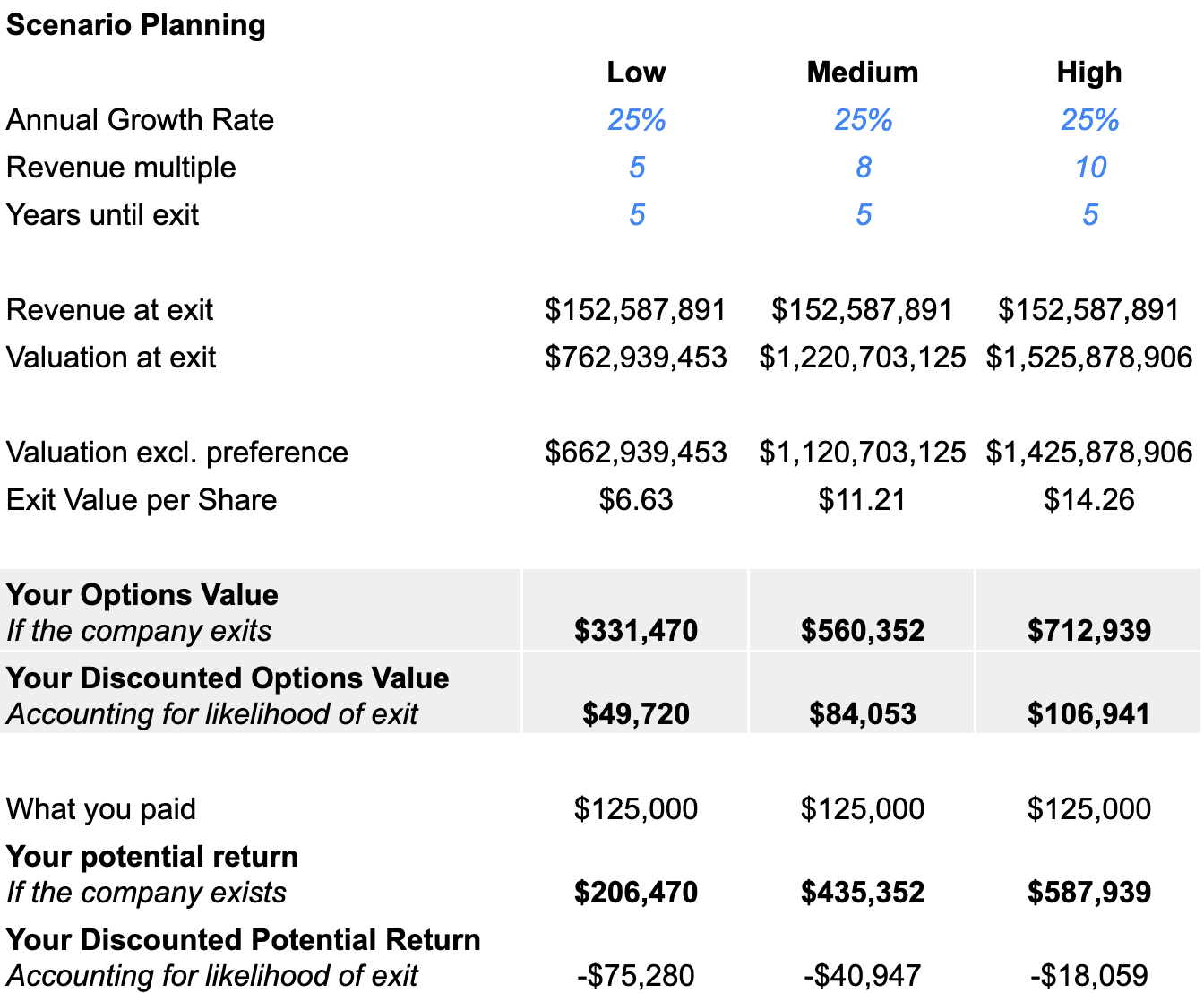

Example: Calculating return for a B2B SaaS company

Here’s an example. You’re leaving a B2B SaaS company – you received 100K options and 50K are vested, so you’re deciding whether to purchase those 50K. According to HR, your company has $100M in preference and 100M shares outstanding.

Your options are priced at $2.50 each, so you could purchase 50K shares for $125,000.

Your company is making $50 million in revenue today and growing at 75% annually, but you’re not sure that will continue, so you assume it will grow an average of 25% per year over the next 5 years.

You run three scenarios of possible revenue multiples – 5x, 8x and 10x.

Plugging these assumptions into the Options Scenario calculator yields three potential returns:

Low case: $206K return

Medium case: $435K return

High case: $588K return

Let’s assume your company has raised a Series C, so multiple these returns by 15% (the likelihood of exit for a Series C company). Now your discounted potential returns are negative, because the cost of your options ($125K) is more than your discounted options value.

Low scenario: -$75K

Medium scenario: -$41K

High scenario: -$18K

Accounting for the likelihood of exit is important, because without this, some or all of your scenarios look exciting – spend $125K and get back $206K-$588K in the future. But remember, all your assumptions have to be true AND the company has to exit for your return to play out.

Step 5: Evaluate the investment and decide

Most people evaluate this decision as an ex-employee. You should evaluate it as an investor.

As an investor, you’d want real conviction that this company will create value for you and your family. This requires having conviction in three areas:

The company will continue to grow quickly

The company will get a high revenue multiple in the market

The company will be acquired or IPO in the next few years

Investors are much more objective than ex-employees. Look for data points like:

Recent exits in your company’s category

Frequency of exits in your company’s category

Exit multiples in your company’s category

Also evaluate the portion of your net capital this investment represents. Investing to purchase these stock options has tradeoffs. You could invest this money elsewhere.

Let’s say you have $25,000 worth of exercisable options – you could write that check to your startup. Or you could take that $25,000 and buy your five favorite tech stocks.

It’s critical you do this analysis through an investor lens because as an ex-employee, your calculus will be more emotional. You’ll say: “I’m sad to leave and want to invest in the company.” Or more likely: “I invested X years of my career into this startup – I don’t want to leave with nothing.”

Our advice

We work for startups in part based on the dream that our equity/stock options will be worth something, and we probably have at least one friend that got lucky and turned their options into meaningful cash.

We’ve all bought into the narrative that stock options are part of our compensation – they’re why we put up with long hours, inexperienced founders/bosses, and pivots. So it’s natural that we want to exercise our options to account for the (very unlikely) event our startup gets acquired or IPOs.

But remember, when you exercise and send a check to your company to buy those options, you are now an investor in the company – and your portfolio likely has just one (or a few) startup investments. Most venture capitalists have hundreds. So you are now a venture capitalist with a VERY small portfolio.

Ultimately, you might decide that’s okay. Maybe you develop conviction as an investor – which means you can see a $50-$100M valuation, healthy growth, and an exit in the future. Or maybe you decide your employee calculus (FOMO or emotional attachment) outweighs your lack of conviction as an investor (and you have some spare cash to burn).

That’s fine. But be upfront and honest with yourself. Right-size your bet to the reason you’re making it. Evaluate that bet vs. other ways you could invest the money. And don’t start shopping for the cabin by the lake.

To the next 10 years,

Greg & Taylor

P.S. Here are a few other factors that can impact this decision. We didn’t cover them in this post, so if these scenarios apply to you, dig deeper.

Exercise Windows – the rules are changing here. 90 day exercise windows remain the norm, but some companies are exploring longer exercise windows (e.g. 12 months). We’d like to see this become the norm. Check your exercise window.

RSUs vs. Stock Options – this post only covers stock options, which are typically for private companies. Some companies (usually public) grant RSUs, which you don’t need to purchase (you own them once you vest). Check whether you have RSUs or options.

Secondary Markets – sometimes, options in later stage companies can be sold pre-acquisition or IPO on a secondary market (here’s an example). Exercising your options and immediately selling your shares on a secondary market allows you to get liquidity and removes the risk your company might not exit. If you work at a later stage company (Series C+), see if there’s a secondary market available.